Calculated Risk has inkling of the possible Bad Bank plan.

I have been back and forth on the Bad Bank idea, and I really hope it works but I am very worried about a give away. At $4 trillion price tag, nationalization sounds more feasible. Obviously, the numbers are going to be politically difficult.

I am somewhat comforted by the fact that Geitner has probably looked at this little manual from Roubini and Setser.

Thursday, January 29, 2009

Supermajortiy

Many sources are stating that the esteemed Senator from New Hampshire may take the post as Commerce Secretary.

This possible placement of a Democrat by the Democratic Governor of New Hampshire with the imminent Franken seating soon will create a Democratic Supermajority in the Senate.

This possible placement of a Democrat by the Democratic Governor of New Hampshire with the imminent Franken seating soon will create a Democratic Supermajority in the Senate.

Friday, January 23, 2009

TARP

Just read the recently released CBO Report on the TARP. There is some very interesting information in this report.

1.) How Much the Government is on the Hook For.

The report details the TARP as of Dec 31, 2008. At that point $247 billion of the $350 billion allocated had been disbursed to about 218 institutions. Based on a Present Value model, the CBO believes the government has subsidized $64 billion (or 26%) of all loans, purchases, and infusions. This means that the $247 billion invested is worth $183 billion today.

2.) How Companies will Pay the Government Back.

An odd characteristic is the structure and repayment scheme. Most are structured in a way that the government purchased preferred shares that pay a dividend (that increases its yield after 5 years), and the government has the ability to convert those shares to common stock at any point in time.

Although that is the most common structure, there is a higher yield from AIG, a different asset warrant structure for part of Citi's injection, and loans to the automakers on different terms.

Throughout the various terms the government will be repaid through dividends, repayment, conversion and sale of common, or a combination of all three.

3.) Success

It seems as though, this program has helped stop the bleeding. Although moral hazard and political influence have run rapid, the financial system has been slowly but surely improving. To be perfectly honest, it is hard to say how far we would have slid without this injection.

And if things improve the government could get much of the money back.

4.) Reforms

(a) First, there needs to be a systematic way to address each and every TARP application. The Citi deal was a complete diversion from the way other institutions have been treated. So, a more coherent policy that is tough and transparent, so banks know where they stand. I do not know exactly what this would look like, but it would not look like the bandage and duck tape system currently in place.

(b) Second, on the accountability and sacrifice front. These companies are all (including the automakers) coming to the government because of bad business decisions and because of an unprecedented financial crisis. These companies should have to give up a considerable amount (like $1.2 million redecorating, yes you John Thain). Oddly enough the only standard that looks close to correct is the one imposed on the automakers. The rules should be adopted should include no dividends, no share repurchases, severely restricted executive compensation, report plans for restructuring, report the on the financial viability of the company (either publicly or to the FED Chair and the Treasury Secretary), and renegotiated severance packages.

Also, the terms on the deals should be much more favorable for the government and the taxpayers. An example is that in exchange for government money, these banks should have to start lending to credit worthy consumers and businesses. This will look like temporary nationalization, but that may be what it will take to jump out of this crisis.

1.) How Much the Government is on the Hook For.

The report details the TARP as of Dec 31, 2008. At that point $247 billion of the $350 billion allocated had been disbursed to about 218 institutions. Based on a Present Value model, the CBO believes the government has subsidized $64 billion (or 26%) of all loans, purchases, and infusions. This means that the $247 billion invested is worth $183 billion today.

2.) How Companies will Pay the Government Back.

An odd characteristic is the structure and repayment scheme. Most are structured in a way that the government purchased preferred shares that pay a dividend (that increases its yield after 5 years), and the government has the ability to convert those shares to common stock at any point in time.

Although that is the most common structure, there is a higher yield from AIG, a different asset warrant structure for part of Citi's injection, and loans to the automakers on different terms.

Throughout the various terms the government will be repaid through dividends, repayment, conversion and sale of common, or a combination of all three.

3.) Success

It seems as though, this program has helped stop the bleeding. Although moral hazard and political influence have run rapid, the financial system has been slowly but surely improving. To be perfectly honest, it is hard to say how far we would have slid without this injection.

And if things improve the government could get much of the money back.

4.) Reforms

(a) First, there needs to be a systematic way to address each and every TARP application. The Citi deal was a complete diversion from the way other institutions have been treated. So, a more coherent policy that is tough and transparent, so banks know where they stand. I do not know exactly what this would look like, but it would not look like the bandage and duck tape system currently in place.

(b) Second, on the accountability and sacrifice front. These companies are all (including the automakers) coming to the government because of bad business decisions and because of an unprecedented financial crisis. These companies should have to give up a considerable amount (like $1.2 million redecorating, yes you John Thain). Oddly enough the only standard that looks close to correct is the one imposed on the automakers. The rules should be adopted should include no dividends, no share repurchases, severely restricted executive compensation, report plans for restructuring, report the on the financial viability of the company (either publicly or to the FED Chair and the Treasury Secretary), and renegotiated severance packages.

Also, the terms on the deals should be much more favorable for the government and the taxpayers. An example is that in exchange for government money, these banks should have to start lending to credit worthy consumers and businesses. This will look like temporary nationalization, but that may be what it will take to jump out of this crisis.

Inauguration

I went to Washington D.C. for the events, more on that nightmare to come. I have returned with a set of renewed refreshed ideas to talk about.

Friday, January 16, 2009

America's BadAsset Bank

There was an announcement yesterday that Sheila Bair (who will stay on as head of the FDIC) and Henry "Hammerin Hank" Paulson have floated the idea of a BadAsset Bank (I made up that name, they said "Bad Bank").

I the surface I think this plan has some merit. With the TED Spread still twice its normal level, and with more housing related losses surely to come, we absolutely need some bold action.

Now, the exact details were not released, but my best guess is that this new entity would work like the trading desk at the FED or at some nameless bank. They would prime the liquidity pump for various frozen markets, and continuously buy and sell toxic assets.

There are surely few positive attributes and opportunities in this plan. One, these assets are probably wildly undervalued, and even if held until maturity the government would end up making a little bit of coin. Two, that the buying and selling of assets or churning (as my former economics professor called it - and which is also illegal for lay people) may make the government money as it does for the Federal Reserve in their buying and selling of Treasuries. Three, most of all banks will be in a be more solvent, and markets more generally will gain confidence. After the Lehman default fear of counterparty default was like a cold chill felt down the spines of all market participants. This phenomenon almost surely gets overblown because not everyone can default, but that's not what credit markets were saying during the throws of the crisis. My guess is this risk would be greatly reduced by this BadAsset Bank, and maybe the progress in credit spreads would continued at an even faster rate.

There are also surely a few negative attributes and opportunities in this plan. First, there is the Krugman concern that the government would waste the money through such a mechanism, and may well pay too much for the toxic assets. Second, there is the size concern, can these markets be affected by such a small amount of money relative to their size. Third, it is possibly that all firms may decide that the creation of the BadAsset Bank would signal a great time to run to the exits, which may further push down asset prices (that said I do not know the likelihood and it may have just the opposite effect).

Now, all of this must be taken in context. I have not seen any draft of this plan, so the details may be operational different than my assumptions and the negatives and risks may be mitigated by the details. My hope is that this idea or something that looks like it, such authority for Treasury or the FED to take on the same responsibilities, are taken seriously. Obviously, the merit in an independent (perhaps emergency) vehicle would be preferable because it would have a more concise, well-defined set of goals and responsibilities than a similar plan in the hands of Treasury or the FED would have.

That is a lot to take in. I surely do not have a comprehensive understanding of the entire idea, but I will try to learn more and synthesize it here in the days to come.

I the surface I think this plan has some merit. With the TED Spread still twice its normal level, and with more housing related losses surely to come, we absolutely need some bold action.

Now, the exact details were not released, but my best guess is that this new entity would work like the trading desk at the FED or at some nameless bank. They would prime the liquidity pump for various frozen markets, and continuously buy and sell toxic assets.

There are surely few positive attributes and opportunities in this plan. One, these assets are probably wildly undervalued, and even if held until maturity the government would end up making a little bit of coin. Two, that the buying and selling of assets or churning (as my former economics professor called it - and which is also illegal for lay people) may make the government money as it does for the Federal Reserve in their buying and selling of Treasuries. Three, most of all banks will be in a be more solvent, and markets more generally will gain confidence. After the Lehman default fear of counterparty default was like a cold chill felt down the spines of all market participants. This phenomenon almost surely gets overblown because not everyone can default, but that's not what credit markets were saying during the throws of the crisis. My guess is this risk would be greatly reduced by this BadAsset Bank, and maybe the progress in credit spreads would continued at an even faster rate.

There are also surely a few negative attributes and opportunities in this plan. First, there is the Krugman concern that the government would waste the money through such a mechanism, and may well pay too much for the toxic assets. Second, there is the size concern, can these markets be affected by such a small amount of money relative to their size. Third, it is possibly that all firms may decide that the creation of the BadAsset Bank would signal a great time to run to the exits, which may further push down asset prices (that said I do not know the likelihood and it may have just the opposite effect).

Now, all of this must be taken in context. I have not seen any draft of this plan, so the details may be operational different than my assumptions and the negatives and risks may be mitigated by the details. My hope is that this idea or something that looks like it, such authority for Treasury or the FED to take on the same responsibilities, are taken seriously. Obviously, the merit in an independent (perhaps emergency) vehicle would be preferable because it would have a more concise, well-defined set of goals and responsibilities than a similar plan in the hands of Treasury or the FED would have.

That is a lot to take in. I surely do not have a comprehensive understanding of the entire idea, but I will try to learn more and synthesize it here in the days to come.

Deflation - On Every Front Imaginable

The ugly head of deflation has once again shown itself, and it scares me quite a bit. Link to latest BLS deflationary CPI. There are two major concerns that I have about deflation.

The first is asset deflation. Housing is the example that has been true for a very long time. People are foregoing the purchase of houses with the knowledge that prices will be less at a future date. This has caused contraction in the housing industry and all industries related to housing (e.g. Construction, Mortgage Banking, Basic Materials). Then, there is the wealth effect on home owners who will spend less because they feel poorer because their house is worth less. There are also externalities in localities and neighborhoods caused by the default and foreclosure phenomenon.

The other asset deflation happened in financial markets. As stocks declined and credit tightened, margin calls ripped through the financial system. This caused individuals, firms, and banks to sell assets to meet margin calls which further caused declines in asset prices. Again this too causes a wealth effect that reduces overall spending.

The second is price deflation or deflation expectations. In his landmark Nobel work on inflation expectations, Milton Friedman showed us that the macroeconomic challenge we faced was not just a trade-off between unemployment and inflation. He posited that when inflation rose too high, inflation expectations would cause stagflation (a period of high inflation and high unemployment). Friedman was bucking the popular trend at the time that if policymakers let inflation rise unemployment would fall. The intuition behind his theory was that as prices rose, workers would demand high wages causing prices to rise further - inflationary expectations causing an inflationary spiral. So, in the 1970s when inflation rose and at a point unemployment began to rise as well, he began his rise to prominence.

Many who are students of the Friedman/Hayek (or Chicago) School of thought, have begun or continued to see the world only through the scope of inflation expectations, but today the real fear should be deflationary expectations. Very similar to the theories and ideas articulated by John Manard Keynes during the Great Depression (some not all). The intuition is very similar to inflationary expectations, just in the opposite direction. When monetary policy makers can no longer effectively increase the money supply (or cause some level of inflation) and when prices are falling they continue to fall. Basically, consumers forgo large portions of consumption with the understanding the prices will fall in the future. This foregone consumption reduces sales, increases inventories, and forces business to close and/or lay-off workers. The greater number of unemployed workers reduces overall demand in the economy which exacerbates the entire deflationary cycle (or spiral).

Can We Prevent Deflation?

My hope is that the multi-front war the Obama Administration plans to fight will make a dent in this cycle. First, the stimulus package which I just hope and pray will be large enough. Second, the TARP money with I hope and pray will stem the foreclosure tide, and renew greater confidence and solvency to the financial system. Third, renewed and restructured financial regulation to bring back confidence in financial markets. Fourth, a large sweeping reform of the health care system to curtail rising costs and stem the bankruptcies directly caused by health care expenses.

I know the TED Spread has narrowed in recent days which means there is less fear in markets, but it is still double the ordinary spread and I think the real economy could cause that fear to come back rather quickly.

We might all need to find religion.

Wednesday, January 14, 2009

Wall Street Journal Poll

A new Wall Street Journal Poll came out.

Obama seems to have his finger on the pulse of the nation.

The most important numbers are his approval rating, the disapproval of the Democratic leadership, and the feeling of the nation on the stimulus.

"Thinking about the economic stimulus legislation, which is a more important priority?

Tax cuts that will allow people to spend more ....... 33

Government spending that will help create jobs.... 63

Not sure .....................................................4"

It seems that the President-Elect either has large amounts of goodwill, or has done a great job of communicating the statitically superiority of certain forms of stimulus he has proposed.

Mr. Ponzi and Mr. Madoff

As the story goes in 1919 Mr. Ponzi decided he could make a killing in a postage rate/currency rate trade, probably similar to modern arbitrage. So confident in his scheme Mr. Ponzi raised funds by promising 50% returns every 45 days (eat your heart out Bernie Madoff), and as one might expect people could not move fast enough to give Mr. Ponzi money.

In just two months his company, the Securities Exchange Company (SEC), went from $1 million raised to over $15 million raised. Realizing he could not make the payments he promised he bought banks, and began piecing the operation together in a form of fraud that would eventually bear his name - Ponzi Scheme. As money came in, it went back out. He robbed Peter to pay Paul.

Eventually he was caught by the U.S. Attorney and the Postal authorities, and pled guily to mail fraud. Mr. Ponzi served 5 years in prison, and eventually wrote an autobiography. I find this selection especially righ because it opitimizes both the mentality that the herd had in the tech bubble, the housing bubble, and the Madoff bubble (or scandal).

"The air was tense with ill-suppressed excitement. Hope and greed could be read in everybody's countenance. Wads of money nervously clutched and waved by thousands of outstretched fists! Madness, money madness, the worst kind of madness, was reflected in everybody's eyes! In a silent exhibition of utter disdain to all principles of calm and careful judgement. In a silent exhibition of the reckless mob psychology, entirely too suceptible to the fatal spell of misguided or perverted leadership!"

This whole story is very much what happen to Bernie Madoff and his investors. Mr. Madoff probably also once had a legitment plan, but probably was very bad as what he did so began to follow in Ponzi's foot steps. Mr. Madoff was a much more shrewd fraud, but the quote from Mr. Ponzi is telling none-the-less. It shows that educated or uneducated, rich or poor, American or European we all get caught up in illogical mob mentality.

For future reference, if it sounds too good to be true it probably is.

Tuesday, January 13, 2009

Hilary Clinton

I am fairly well versed in economic and domestic policy issues, but I know a great strategic foreign policy thinker when I see one - and Hillary Clinton is just that.

Listening and watching her answer questions is a astounding show of intelligence, confidence, and competence. She has answered questions on development as a tool of foreign policy, synergy between the military and diplomat complexes, Iran, nuclear proliferation, Russia/Ukraine, women's rights, management style, and State Department funding.

I feel good about our prospects of a more collaborative international community.

Monday, January 12, 2009

Reform

It strikes me as odd that both the incoming administration and the political elites have not taken bold stances in this dire time. Across the board I have been surprised at the fickle rhetoric of both the Obama Administration, the President-Elect himself, and Democrats on the Hill.

Republicans may be consistently wrong about economic issues, but they are relentless in their pursuant of incorrect policies. Democrats would rather take a bad comprimise than a principled tough win, that just happens to be good policy as well.

Much of this is difficult to discern considering that they have little power until next Tuesday, but it has been a trend the last few weeks. I look forward to a change in tone and principled positions next week.

Can We Spend Enough Money?

There are plenty of projects out there that need to be pursued:

- Roads

- Bridges

- Broadband lines

- Schools

- Green Federal Building

But my worry is not that we will spend too much, but that we will spend to little, below are a few other projects to be taken up, a few statistics, and my view summarized.

- Light Rail Projects (suburban to urban)

- High Speed Rail Projects

- Spending to fight childhood poverty

- Smart Grid

- Health Care Reform

But lets get the most bang for our buck short and long-term:

Friday, January 9, 2009

TARP

First of all we should all agree that Congress sucks at naming things. TARP or Troubled Asset Relief Program.

I just watched Barney Frank on Bloomberg, and he will be releasing all the details of the improved TARP legislation this afternoon. From is comments all the signs are encouraging. More accountability, more money getting to community banks, money available for Treasury to by Municipal bonds to lower Municipalities borrowing costs, $40 to $100 billion for foreclosure prevention, and much more.

Most of this is spot on. Paulson and the folks in the Bush Administration have failed on many levels during this crisis, but the direction of relief is the largest amongst these failures. During 2007 and/or 2008 they should have taken bold action in the housing market to keep people in their homes and renegotiate their mortgages. Although a 21st century run on the bank and loss of confidence in the CDO, MBS, and other derivative markets were the front page story. What under lied this panic was actual defaults and foreclosures by actual people. So, if they would have stepped up earlier to stem the homeowner tide or mitigate the necessary losses much damage may have been avoided.

The foundation of this rationale is that banks only get about 50% of the money back on a foreclosed property - and as far as I know this number does not include administrative costs which are considerable. And CDO and MBS markets (this number is based on what I remember from memory, ill try to find the actual) have dropped some 60 to 70% at certain points. This means renegotiation would be beneficial in many instances for both the homeowner and the investor. I give you the Sheila Bair plan.

This plan is absolutely necessary, my hope it only that Tim Geitner and his staff are bold enough. If they can create a workable model like the Bair plan estimates are that 1/3 or 1/2 of foreclosures can be avoided. This urgency of this plan is not only the havoc more defaults and foreclosures could reap on financial markets, but also the externalities experienced by affected communities.

I drove down a 16 house street the other day with 9 vacant foreclosures houses. First and foremost those other 7 families are in trouble because this much vacancy lowers their home values and makes it all but impossible to sell their homes. It creates an fertile ground for criminals and desperate unemployed people to steal from those vacant homes and/or tear apart the inside and outside of the house. Without a community cooperative effort houses will degrade and yards will not be mowed. The lose in property taxes will force budget cuts in essential services like police, fire, and education.

The long and short of all this is that Barney Frank and Co. are on the right track with their vision for the last $350 of the TARP, but it must be used boldly, intelligently and then lets just hope we do not need TARP II. Even with bold action something tells me TARP II is just around the corner.

Thursday, January 8, 2009

A Debate Perhaps?

Congressional Democrats led by Kent Conrad have begun to raise doubts today about the massive tax cuts offered in the latest leak of the Obama plan. This is an encouraging development, because the President-elect must have his own party on board first. The majority of the comments raise doubts about tax cuts relative to infrastructure spending in their effectiveness or "Bang for the Buck."

On a historical note, this development is quite similar to FDR's New Deal. The part of New Deal history that usually goes untold or undertold is that it was congressional Democrats, and not FDR, who were the catalyst of truly progressive economic policy. FDR was of course their voice, but in reality he was was much more moderate than the programs indicate. My guess is the debate then sounded quite similar to the debate now, lets just hope we learned from history. By that I mean that the stimulus should be larger as a percent of GDP than was the WPA (along with other New Deal programs) that were never quite large enough to give the economy the jolt it needed.

FDR and Obama both spoke in a tone that trumpeted BOLD action, but in reality it is Congress and not moderate Presidential positions that will actually be the catalyst for such action. I do not actually think this is a bad thing. I believe that the leader of the free world should be a Radical Moderate, meaning he or she should be the person asking tough questions and pushing the ideological assumptions of both the right and the left.

Wednesday, January 7, 2009

Disappointment

I would be considered in most circles to be a left of center moderate, with a bias towards facts and objective opinion. But this fiscal stimulus debate has been completely disappointing and disconcerting so far. My hope is that the posturing is politics and the end result will be positive.

My major qualm has been the Obama team's blind ignorance to facts. There are some who say this stimulus plan is diverse to stimulate the economy in different way through all avenues. The facts say something far different.

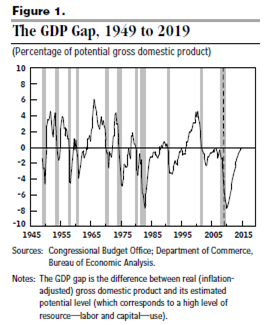

There are a few problems, one as this graph from the CBO via Paul Krugman shows, there is an output gap. Meaning the economy is functioning about 8% below capacity. Monetary policy is at the zero bound and fiscal policy needs to stimulate demand.

This is dire because just like the psychology involved in bubbles, during deep recessions there is a self-reinforcing adverse psychology pushing everything lower.

With that in mind the best one can hope for is big, drastic fiscal stimulus done in the most efficient, effective manner. And flat out, the Obama proposals do not seem to be the most effective "Bang for the Buck" according to Marc Zandi (Refer to Page 3). When Zandi ran the numbers the three most effective sources of fiscal stimulus per dollar were:

- temporary increase in food stamps - 1.73

- extend unemployment insurance benefits - 1.64

- increase infrastructure spending - 1.59

the three least effective sources were:

- accelerated depreciation - 0.27

- extending the Bush tax cuts - 0.29

- cut corporate taxes - 0.30

And the Obama team seems wiling to make these sorts of tax cuts a major portion of the legislation. And why? So, they can run up 80 votes in the Senate. Although the comparison is not completely symmetric, LBJ helped pass a toothless Civil Rights act before 1964 and 1965 because he made it a compromise bill. The Obama team seems to be willing to do the same with a bad fiscal stimulus plan - bad is the correct term because it is a waste of taxpayer money not to send money to the most efficient, effective use.

When the fiscal stimulus is voted on, the Obama teams and Democrats will have 59 seats in the Senate and a tidal wave of public support behind them. Why pass a bad compromise bill? When they could pass a great piece of legislation with 60 votes.

How do I know this outline of legislation is bad. One, the quantitative numbers from Zandi (who by the way actually likes the Obama plan) and other sources show quite clearly the most effective sources for stimulus especially in a period of aggregate demand shock (tax cuts provide supply not demand). Two, the average estimate from professional economists, stimulus included, is that unemployment will peak at 8.4% and that growth will resume in December or so, but that once growth resumes it will resume at a slow rate.

This fiscal stimulus gives the Obama team to grow public support for progressive policy and the opportunity to do what is right for the economy. However, their willingness to provide half measure when full are needed (see Japan in the 1990's) will end up not stimulating the economy as is needed and will end up hurting them politically when we have sclerotic growth in 2010.

I hope I am wrong, but if this opportunity is lost another may not be found again.

Sunday, January 4, 2009

Sixteen Days

An old friend of mine recently passed away. Because of his passing many old friends have talked to me about him and about their lives.

The thing that I am hearing again and again is how fast the economy is slowing, and how quickly the labor market is deteriorating (even though this qualitative evidence is not perfect, it is something). President-Elect Obama takes office in sixteen days, and very soon after a stimulus package will be signed into law. But based on what I am hearing, I am truly worried about the prospects because of TIME. First, sixteen days is a long time so Governors better have their infrastructure personelle hired and in place. Second, much of the spending effects will not be felt until June, July, August, or September.

I truly hope credit markets gain confidence soon, or we could be in for a rough few months. The next five months could be the difference between three percent decline in GDP and a six pecent decline in GDP.

Friday, January 2, 2009

Little Break ... Lets Talk a Little about Productivity Growth

After a couple day break, and some much needed rest and relaxation, my perspective and ability to see things clearly have been greatly improved.

Today, I watched Paul Volcker on charlierose.com (Volcker has been on some 5 or 6 times since 1997). The first interview was the central banking legend talking about the economy in 1997. First and foremost, what vision the man had as he talked positively about the prospects of the economy which would boom 1998-2000. The second point that caught my attention was his point about productivity growth.

(The paragraphs to follow are estimates based on numbers I have seen, and I will try to follow with more well-defined facts and sources tomorrow.)

Since 1979 there have been only about 6 or 7 years of outstanding productivity growth and in turn economic growth. By my best estimate they would be 1983-1985, 1988, and 1997-1999. If one looks at the prior 30 years the productivity growth and economic growth numbers were considerably better.

Why?

On the economic growth side a factor that may contribute by about one percent is population growth as an input to economic growth, once the boomer generation was done entering the labor force that input declined.

Another important factor was one articulated by Mr. Volcker in his interview, and that is measuring productivity growth. By his estimation (and I partly agree), an industrial based manufacturing economy was easier to measure than a service based economy. Inputs and Outputs are much easier to measure when it is machines rather than content on paper.

I would argue two additional points. One, that the G.I. Bill and other educational spending ushered in an era of greater productivity growth and technological advance. Two, that New Deal liberalism and progressive policies ushered in shared prosperity and higher incomes for middle and lower income families. This increase in wages was broadly an incentive to work harder and increase productivity at a faster clip. Another piece of that New Deal policy ideal is that of broader macroeconomic measures, and most specifically health care spending as a percentage of GDP. Below is a nice graph I grabbed from Paul Krugman based on information he got from CMS.

This health care problem affects the United States in three ways.

First, it is like a tax on firms to come to the United States because of health care. In other words health care makes us less competitive, anecdotely there has been a Dell Call Center I heard about recently built in Ireland and a Honda plant built in Canada. I'm sure that wasn't the only reason, but it was the reason cited.

Second, is overall health and wellness of the workforce. The World Economic Forum's Global Competitive Index uses this as a parameter, and it seems logical that a healthier workforce might to some extent be a more productive workforce.

Third, is the crowding out that can be seen in the graph above. Conservatives often make the argument that "big government" spending crowds out private investment (which is plausible and has happen), but recently health care spending has crowded out private and public investment in much the same way. In other words every dollar spent on health care is a dollar not spent on R and D in the automobile industry or really an industry of your choosing.

Does it Matter?

One argument most critics of my argument would make is that the lower productivity growth numbers have been offset by longer more protracted periods of modest growth. So, eight years of modest growth and a shallow recession is better than six years of large growth and a fairly large recession. It is hard to say how plausible that argument is, but it seems to me that in the 1950's and 1960's we had both large growth and fairly modest recessions.

Conclusion

This is an interesting topic of discussion, especially in a period of time in which the decline in GDP will be unparalleled since the Great Depression. This couple with the fact that many economists worry that the recovery in 2010 and beyond could mirror the lost decade Japan experienced in the 1990's if policy makers do not handle the situation effectively.

There are more serious issues to address right now, but it seems to me that if the fiscal stimulus is done right we could get some measure in it that could mirror policies of the success post-war boom era.

Today, I watched Paul Volcker on charlierose.com (Volcker has been on some 5 or 6 times since 1997). The first interview was the central banking legend talking about the economy in 1997. First and foremost, what vision the man had as he talked positively about the prospects of the economy which would boom 1998-2000. The second point that caught my attention was his point about productivity growth.

(The paragraphs to follow are estimates based on numbers I have seen, and I will try to follow with more well-defined facts and sources tomorrow.)

Since 1979 there have been only about 6 or 7 years of outstanding productivity growth and in turn economic growth. By my best estimate they would be 1983-1985, 1988, and 1997-1999. If one looks at the prior 30 years the productivity growth and economic growth numbers were considerably better.

Why?

On the economic growth side a factor that may contribute by about one percent is population growth as an input to economic growth, once the boomer generation was done entering the labor force that input declined.

Another important factor was one articulated by Mr. Volcker in his interview, and that is measuring productivity growth. By his estimation (and I partly agree), an industrial based manufacturing economy was easier to measure than a service based economy. Inputs and Outputs are much easier to measure when it is machines rather than content on paper.

I would argue two additional points. One, that the G.I. Bill and other educational spending ushered in an era of greater productivity growth and technological advance. Two, that New Deal liberalism and progressive policies ushered in shared prosperity and higher incomes for middle and lower income families. This increase in wages was broadly an incentive to work harder and increase productivity at a faster clip. Another piece of that New Deal policy ideal is that of broader macroeconomic measures, and most specifically health care spending as a percentage of GDP. Below is a nice graph I grabbed from Paul Krugman based on information he got from CMS.

This health care problem affects the United States in three ways.

First, it is like a tax on firms to come to the United States because of health care. In other words health care makes us less competitive, anecdotely there has been a Dell Call Center I heard about recently built in Ireland and a Honda plant built in Canada. I'm sure that wasn't the only reason, but it was the reason cited.

Second, is overall health and wellness of the workforce. The World Economic Forum's Global Competitive Index uses this as a parameter, and it seems logical that a healthier workforce might to some extent be a more productive workforce.

Third, is the crowding out that can be seen in the graph above. Conservatives often make the argument that "big government" spending crowds out private investment (which is plausible and has happen), but recently health care spending has crowded out private and public investment in much the same way. In other words every dollar spent on health care is a dollar not spent on R and D in the automobile industry or really an industry of your choosing.

Does it Matter?

One argument most critics of my argument would make is that the lower productivity growth numbers have been offset by longer more protracted periods of modest growth. So, eight years of modest growth and a shallow recession is better than six years of large growth and a fairly large recession. It is hard to say how plausible that argument is, but it seems to me that in the 1950's and 1960's we had both large growth and fairly modest recessions.

Conclusion

This is an interesting topic of discussion, especially in a period of time in which the decline in GDP will be unparalleled since the Great Depression. This couple with the fact that many economists worry that the recovery in 2010 and beyond could mirror the lost decade Japan experienced in the 1990's if policy makers do not handle the situation effectively.

There are more serious issues to address right now, but it seems to me that if the fiscal stimulus is done right we could get some measure in it that could mirror policies of the success post-war boom era.

Subscribe to:

Posts (Atom)